$4 Billion in Tanker Exposure

The security environment in the Persian Gulf has undergone a fundamental structural shift following the escalation that began on February 28, 2026. For the (re)insurance market, the Strait of Hormuz has transitioned from a high-risk transit corridor to an active conflict zone, resulting in a near-total suspension of commercial traffic and a critical concentration of hull and cargo exposure.

The escalation of hostilities in the Persian Gulf since 28 February 2026 has fundamentally altered global maritime risk patterns. With the Strait of Hormuz effectively closed to commercial shipping, insurers are now confronting one of the largest geographic redistributions of energy transport risk in modern shipping.

Under normal conditions, nearly 20 million barrels per day of crude oil and petroleum products move through the Strait of Hormuz, representing roughly a quarter of global seaborne oil trade and around 20% of global oil consumption.

The near suspension of shipping has therefore disrupted the world’s most critical energy chokepoint and forced Gulf producers to activate overland export infrastructure designed specifically to bypass the Strait.

This infrastructure is now functioning as the global energy system’s “supply balancer.”

The Supply Balancer: Oil Moving Overland

The primary pipelines currently sustaining Gulf exports are:

- Saudi Arabia’s East–West Petroline to the Red Sea terminal at Yanbu

- The UAE’s Habshan–Fujairah pipeline (ADCOP) to the Gulf of Oman

Together, these pipelines provide approximately 6.5 – 7.0 million barrels per day of bypass capacity, allowing crude exports to reach global markets without transiting the Strait of Hormuz.

Given that around 20 million barrels per day normally transit the Strait, these alternative routes currently allow roughly 30-33% of Gulf oil exports to move overland.

In practical terms, this means:

- Around one-fifth of Gulf oil exports are now moving across land rather than by tanker through Hormuz.

- The remaining volumes are either temporarily shut in, stored, or awaiting maritime clearance.

For energy markets, this pipeline network acts as a pressure valve, preventing a complete collapse of global supply.

For insurers, however, it is creating new maritime risk concentrations at the export points where these pipelines terminate.

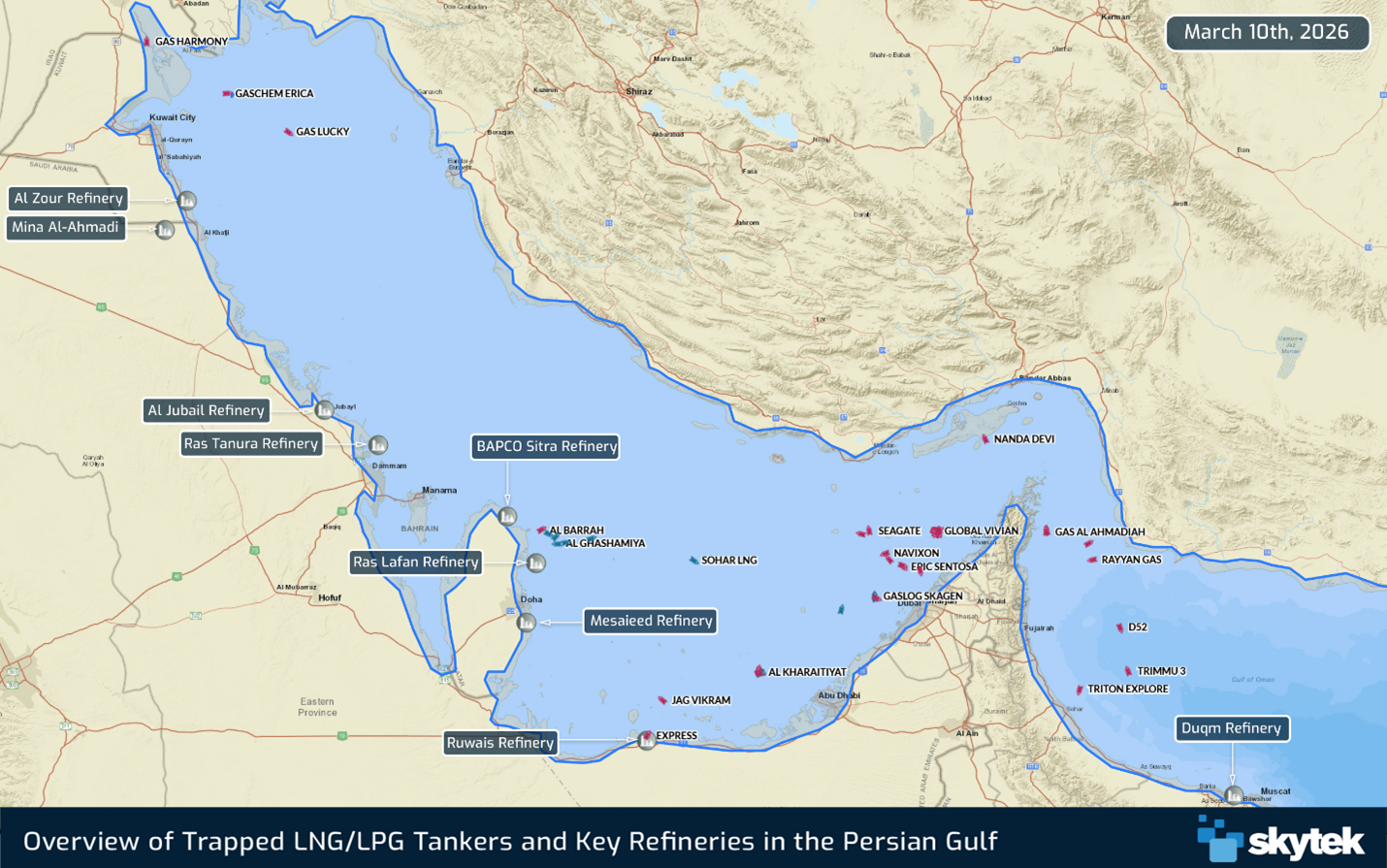

Yanbu: The New Global Export Node

The largest shift in tanker traffic is occurring at Yanbu, Saudi Arabia’s Red Sea export terminal.

Crude transported via the East–West Petroline now arrives at Yanbu, where it is loaded onto VLCCs for shipment to Europe and Asia. With the pipeline operating near maximum capacity, the port has rapidly become the primary maritime outlet for Gulf oil, bypassing the Strait of Hormuz.

This shift has several implications for marine insurers:

- Accumulation risk

Large crude carriers carrying cargoes worth, on average, $100 million each are now clustering in a relatively small anchorage zone. A queue of just 10 vessels could represent over $2 billion in insured hull and cargo value. - Concentration of high-value assets

The sudden surge in traffic is creating port-level accumulation exposure rarely seen in the Red Sea energy corridor. - Expanded threat geography

While Yanbu lies outside the Persian Gulf, it remains within the operational reach of long-range drone and missile systems, meaning the concentration of tankers represents a potential multi-billion-dollar risk cluster.

For insurers, the key takeaway is that maritime risk has migrated westward rather than diminished.

Fujairah: Outside the Strait, Not Outside the Conflict

The UAE’s Habshan–Fujairah pipeline provides another bypass route, transporting crude from Abu Dhabi to the Fujairah export terminal on the Gulf of Oman.

With a capacity of roughly 1.5–1.8 million barrels per day, the pipeline allows UAE exports to reach international markets without entering the Strait of Hormuz.

However, recent strikes on energy infrastructure in Fujairah illustrate a critical shift in the risk environment.

Historically, loading terminals outside the Strait were considered lower-risk alternatives. The current conflict suggests that the distinction may no longer hold.

Strategic Implications for the Insurance Market

The closure of Hormuz has triggered a dramatic geographic redistribution of maritime energy risk.

Three key exposure zones are now emerging:

- Red Sea export terminals – 29 tankers over $ 1.5 bn in hull value accumulation at Yanbu

- Gulf of Oman terminals – infrastructure exposure at Fujairah, Sohar, and Duqm.

- The Persian Gulf interior – over 700 merchant ships, exceeding $ 21 bn vessels trapped inside the blockade zone

At the same time, tanker routes between Asia and Europe are increasingly diverting around the Cape of Good Hope, adding 10–14 days to voyage durations and increasing insured exposure values for both hull and cargo.

For the marine insurance market, the central challenge is no longer just the closure of a strategic chokepoint.

It is the rapid reallocation of billions of dollars in maritime assets toward new export hubs that were never designed to absorb this level of traffic.

In this new environment, real-time monitoring of vessel clustering and port accumulation risk will be critical for managing marine hull, cargo, and war-risk portfolios.